If you’ve been frustrated by the lack of homes for sale over the past few years, here’s some good news. You have more options, so it may finally be time to kick off your home search again. As Daryl Fairweather, Chief Economist at Redfin, explains:

“Now is the best time to buy in the last two years. Mortgage rates are comparable to what they were two years ago, and prices remain high. However, there is significantly more inventory . . .”

The number of homes for sale has grown compared to last year, and even more options are on the way. While this is typical for the busy spring season, here’s why this is so important right now.

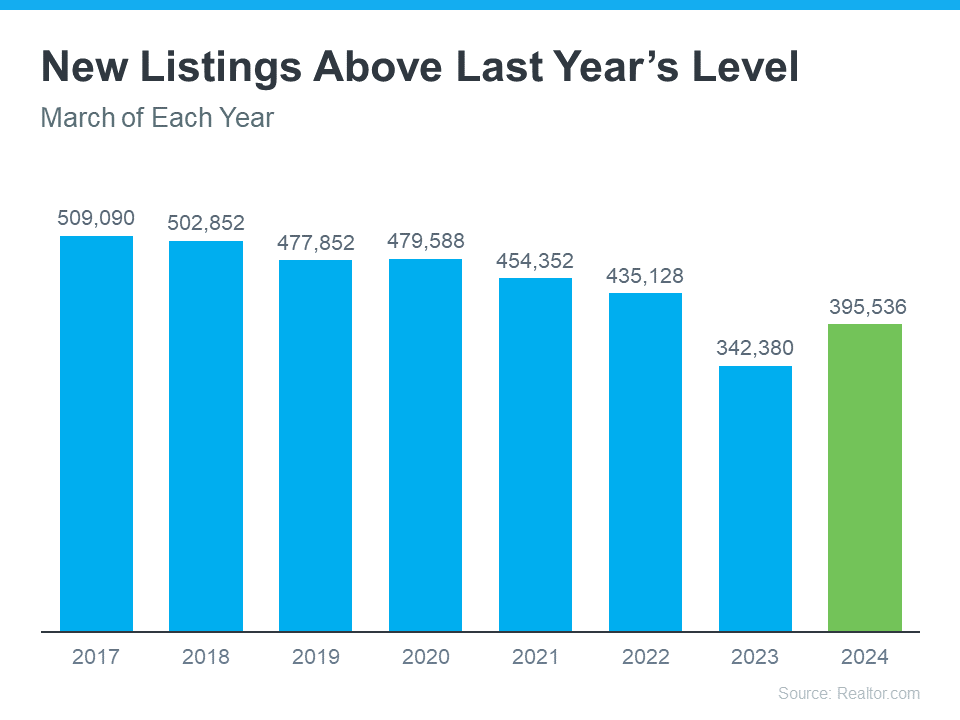

Homeowners are listing their houses at the highest pace we’ve seen in a while.

Over the past few months, the number of new listings, or homes that have recently been put on the market for sale, has been steadily rising (see graph below):

Basically, more people are putting their homes on the market each month – whether they’re moving up, downsizing, or relocating. And this trend is a positive sign for the housing market.

Sellers who may have been on the fence the past few years are starting to jump back in. That’s helping to boost overall inventory and create better opportunities for both buyers and move-up sellers alike.

But it’s not just that the number of fresh options is up month-over-month; there’s also been a jump compared to last year.

According to Realtor.com, new listings in March were 10.2% higher than last year, making it the biggest March for new listings since 2021 (see graph below):

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

To make sure you don't miss out on any of the latest listings for your area, lean on a local real estate agent.

If you're thinking about making a move this spring, now may be the time to start exploring your options. With more fresh listings hitting the market, you may find a home you love waiting for you.

What features or neighborhoods are at the top of your wish list?

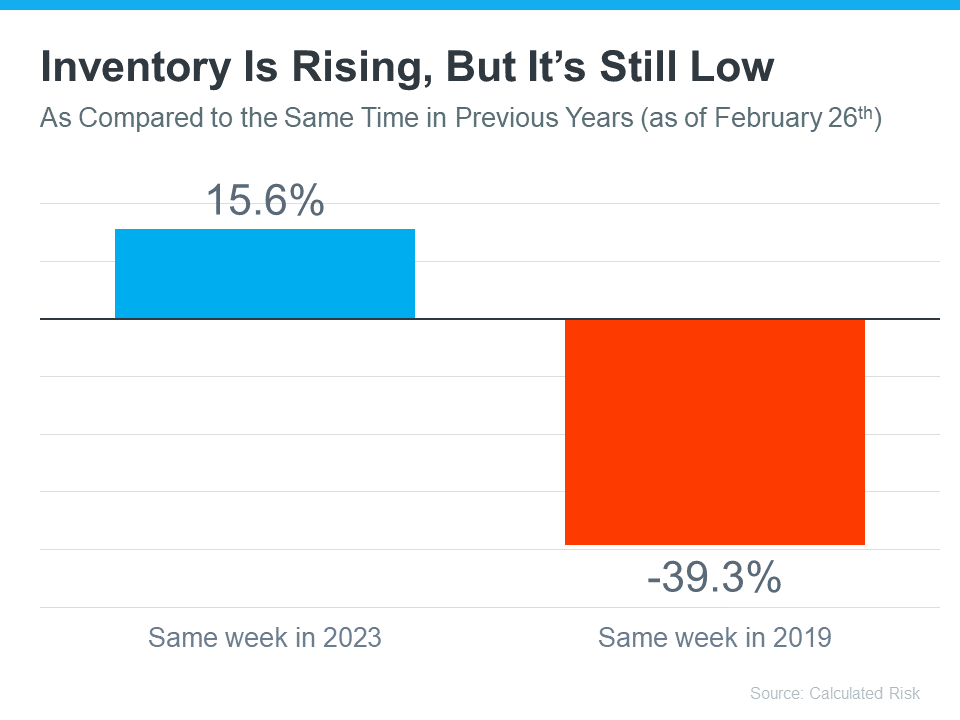

A few years ago, inventory hit a record low. Just about anything sold – and fast. But now, there are far more homes on the market. Listings are up almost 20% from this time last year. And in some areas, supply is even back to levels we last saw in 2017–2019. For sellers, that means one thing:

Your house needs to stand out and grab attention from day one.

That’s especially true when you consider why the number of homes for sale is up. Here’s how it works. Available inventory is a mix of:

Active Listings: homes that have been sitting on the market, but haven’t sold yet

New Listings: homes that were just put on the market

Data from Realtor.com shows most of the inventory growth lately is actually from active listings that are staying on the market and taking longer to sell (see the graph below).

The blue bars show active listings. These are the homes that are sitting month to month and not selling. The green bars are new listings, the homes that were just put on the market. And it’s clear there are fewer new listings compared to how many are staying on the market unsold.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

The secret to selling in today’s market is simple. Make sure your house is easy for buyers to say yes to as soon as it is listed.

Price it based on current conditions (not what your neighbor sold for 3 years ago). Make important repairs. And highlight the best things about your house. If you do that, it will sell in any market – sometimes even faster than you’d think. Because the truth is, homes that are priced right today are still selling.

It’s the homeowners who are clinging to outdated expectations that are seeing their house sit and their listing go stale. According to Redfin and HousingWire, here are some of the most common reasons sales stall out:

Priced it too high from the start

Skipped necessary repairs before listing

Didn’t stage the house well

Sellers won't negotiate with buyers

Limited availability for showings

Ineffective marketing or listing pictures

Most of those things didn’t matter as much just a few years ago. When inventory was at a record low, sellers could skip the prep, name their price, and still walk away with multiple offers over their asking price.

But today’s market is different now that inventory has grown. And that means your approach needs to be different too.

You don’t want to try out old strategies and aim too high just to see what sticks. Your first few weeks on the market are everything. That’s when your listing gets the most attention – and when pricing or presentation mistakes hurt the most. Get it wrong up front and your house will sit...and sit. Get it right, and it’ll be snatched up before you know it.

Selling quickly isn’t about luck. It’s about knowing how to play to the market you’re in. And that’s where your agent comes in.

A great agent will analyze your local market, suggest a price based on the latest comparables sold in your neighborhood, and create a marketing plan that makes buyers pay attention from day one. They’ll also walk you through any repairs you need to make or whether you need to bring in a staging company. As the National Association of Realtors (NAR) explains:

“Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home.”

That’s the power of getting it right (and getting expert help) from the start.

There are more homes for sale today than there were even just a year ago, but that doesn’t have to work against you.

When your house is priced right, shows well, and is marketed effectively, it will sell. Let’s connect if you want to know how to make that happen in our market this fall.

If you’ve seen headlines or social posts calling for a housing crash, it’s easy to wonder if home values are about to take a hit. But here’s the simple truth.

The data doesn’t point to a crash. It points to slow, continued growth.

And sure, it’s going to vary by local area. Some markets will see prices rise more than others. And some may even see small, short-term declines. But the big picture is: home prices are expected to rise nationally, not fall, over the next 5 years.

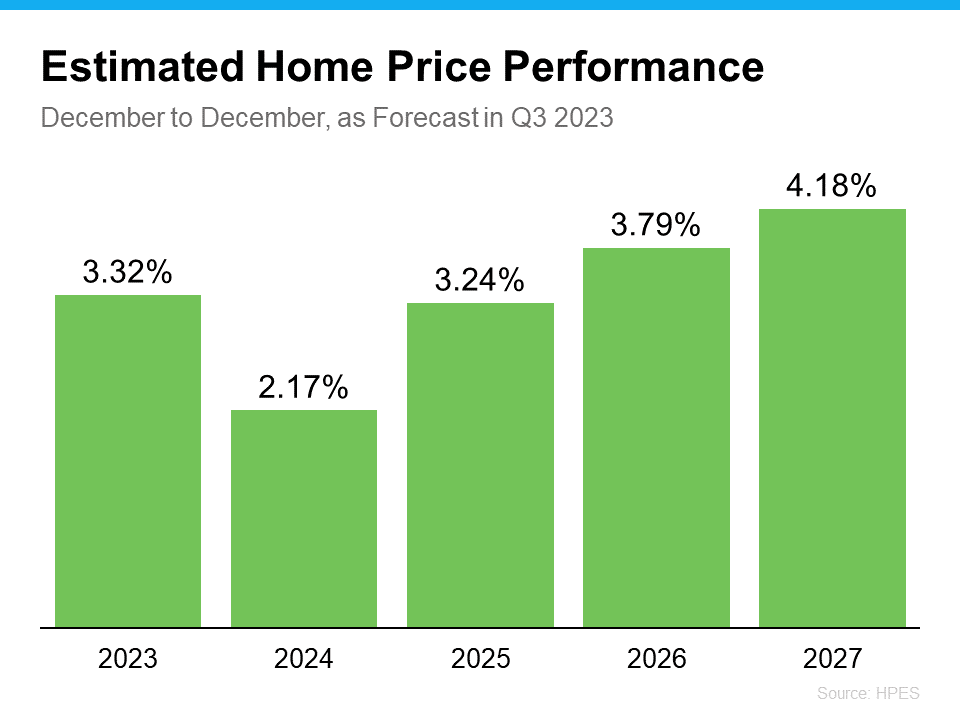

In the Home Price Expectations Survey (HPES) from Fannie Mae, each quarter over 100 leading housing market experts weigh in on where they project home prices will go from here. And in the report that was just released, the experts agree prices are projected to climb nationally through at least 2029 (see graph below):

Here’s how to read this visual. Each bar in that graph shows an increase, not a loss. It’s just that the anticipated pace of that appreciation varies year-to-year.

And to further drive this home, let’s look at another view of where prices are and where they’re expected to go. In this version, the expert forecasts are broken into 3 categories: the overall average, the most optimistic projections, and the most pessimistic projections (see chart below):

Notice how even the most pessimistic forecasters say we’ll see prices rise by almost 5% over the next few years.

Overall, prices are expected to rise about 15% from now through the end of 2029. The optimists say we’ll beat that and see a roughly 26% increase. And even the pessimists anticipate prices will go up by 5% during that period.

What sticks out the most? None of these groups who study the market are forecasting a crash, or even a decline, over the next 5 years.

Now, focus back on the first graph. The projections call for 2-3.5% price increases in each of the next five years. For context, the average rate of appreciation for the last 25 years was closer to 4-5% annually.

So, while that’s slightly below the historical average, it’s much more sustainable and typical than where the market was in 2020, 2021, and 2022.

Back then, prices rose too much, too fast based on record-low supply and record-high demand. Some places even saw prices climb by 15-20%.

So, while it may feel like prices are stalling compared to those pandemic-era surges, what’s really happening is that the market is finally finding balance again.

A lot of the chatter about home prices today is based on that rapid rise and the old saying that what goes up, must come down. But historically, that’s not really true. Home prices almost always rise.

And the main reason we’re not heading for a repeat of 2008 is simple: supply and demand.

Even though affordability challenges have made it harder for some people to buy over the past few years, there still aren’t enough homes for everyone who wants one. And that ongoing shortage is keeping upward pressure on prices nationally.

That’s why experts across the board can confidently agree: we’re not headed for a price collapse, but for steady, long-term appreciation.

And just in case it’s the economy that’s got you worried, remember this. Over the past 50 years, there have been plenty of economic events that have impacted the market. And one thing that’s consistently been true throughout time is the housing market always recovers. And we’re coming through that turn right now and going into a recovery.

If you’ve been waiting to buy or sell because you’re worried about a crash, it’s time to look at the data – not the headlines.

The question isn’t if home prices will rise, it’s by how much.

Let’s connect so you know what’s happening in our local market and what these forecasts mean for your next move.

After a couple of years where the housing market felt stuck in neutral, 2026 may be the year things shift back into gear. Expert forecasts show more people are expected to move – and that could open the door for you to do the same.

With all of the affordability challenges at play over the past few years, many would-be movers pressed pause. But that pause button isn’t going to last forever. There are always people who need to move. And experts think more of them will start to act in 2026 (see graph below):

What’s behind the change? Two key factors: mortgage rates and home prices. Let’s dive into the latest expert forecasts for both, so you can see why more people are expected to move next year.

The #1 thing just about every buyer has been looking for is lower mortgage rates. And after peaking near 7% earlier this year, rates have started to ease.

The latest forecasts show that could continue throughout 2026, but it won’t be a straight line down (see graph below):

There’s a saying: when rates go up, they take the escalator. But when they come down, they take the stairs. And that’s an important thing to remember. It’ll be a slow and bumpy process.

Expect modest improvement in mortgage rates over the next year but be ready for some volatility. There will be volatility along the way as new economic data comes out. Just don't let it distract you from the bigger picture: the overall trend will be a slight decline. Forecasts say we could hit the low 6s, or maybe even the high 5s.

And remember, there doesn't have to be a big drop for you to feel a change. Even a smaller dip helps your bottom line.

If you compare where rates are now to when they were at 7% earlier this year, you’re already saving hundreds on your future mortgage payment. And that’s a really good thing. It’s enough to make a real difference in affordability for some buyers.

What about prices? On a national scale, forecasts say they’re still going to rise, just not by a lot. With rates down from their peak earlier this year, more buyers will re-enter the market. And that increased demand will keep some upward pressure on prices nationally – and prevent prices from tumbling down.

So, even though some markets are already seeing slight price declines, you can rest easy that a big crash just isn’t in the cards. Thanks to how much prices rose over the last 5 years, even the markets seeing declines right now are still up compared to just a few years ago.

Of course, price trends will depend on where you are and what’s happening in your local market. Inventory is a big driver in why some places are going to see varying levels of appreciation going forward. But experts agree we’ll see prices grow at the national level (see graph below):

This is yet another good sign for buyers and overall affordability. While prices will still go up nationally, it’ll be at a much more sustainable pace. And that predictability makes it easier to plan your budget. It also gives you peace of mind that prices won’t suddenly skyrocket overnight.

After a quieter couple of years, 2026 is expected to bring more movement – and more opportunity. With sales projected to rise, mortgage rates trending lower, and price growth slowing down, the stage is set for a healthier, more active market.

So, the big question: will you be one of the movers making 2026 your year?

Let’s connect if you want to get ready.

You want mortgage rates to fall – and they've started to. But is it going to last? And how low will they go?

Experts say there’s room for rates to come down even more over the next year. And one of the leading indicators to watch is the 10-year treasury yield. Here's why.

For over 50 years, the 30-year fixed mortgage rate has closely followed the movement of the 10-year treasury yield, which is a widely watched benchmark for long-term interest rates (see graph below):

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down.

It’s been a predictable pattern for over 50 years. So predictable, that there’s a number experts consider normal for the gap between the two. It’s known as the spread, and it usually averages about 1.76 percentage points, or what you sometimes hear as 176 basis points.

Over the past couple of years, though, that spread has been much wider than normal. Why? Think of the spread as a measure of fear in the market. When there’s lingering uncertainty in the economy, the gap widens beyond its usual norm. That’s one of the reasons why mortgage rates have been unusually high over the past few years.

But here’s a sign for optimism. Even though there’s still some lingering uncertainty related to the economy, that spread is starting to shrink as the path forward is becoming clearer (see graph below):

And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains:

“A lower mortgage spread equals lower mortgage rates. If the spread continues to decline, mortgage rates could fall more than they already have.” The 10-Year Treasury Yield Is Expected To Decline

It’s not just the spread, though. The 10-year treasury yield itself is also forecast to come down in the months ahead. So, when you combine a lower yield with a narrowing spread, you have two key forces potentially pushing mortgage rates down going into next year.

This long-term relationship is a big reason why you see experts currently projecting mortgage rates will ease, with a fringe possibility they’ll hit the upper 5s toward the end of next year.

Here's how it works. Take the 10-year treasury yield, which is sitting at about 4.09% at the time this article is being written, and then add the average spread of 1.76%. From there, you’d expect mortgage rates to be around 5.85% (see graph below):

But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

How these dynamics play out will depend on where the economy, the job market, inflation, and more go from here. But the 2026 outlook is currently expected to be a gradual mortgage rate decline. And as of now, things are starting to move in the right direction.

Keeping up with all of these shifts can feel overwhelming. That’s why having an experienced agent or lender on your side matters. They’ll do the heavy lifting for you.

If you want real-time updates on mortgage rates, let's connect so you have someone to keep you in the loop and help you plan your next move.

If you’re planning to buy a home this year, there’s one expense you can’t afford to overlook: closing costs.

Almost every buyer knows they exist, but not that many know exactly what they cover, or how different they can be based on where you're buying. So, let’s break them down.

Your closing costs are the additional fees and payments you make when finalizing your home purchase. Every buyer has them. According to Freddie Mac, they typically include things like homeowner insurance and title insurance, as well as various fees for your:

Loan application

Credit report

Loan origination

Home appraisal

Home inspection

Property survey

Attorney

When you search for information about closing costs online, you’ll often see a national range, usually 2% to 5% of the home’s purchase price. While that’s a useful starting point if you’re working on your homebuying budget, it doesn’t tell the whole story. In reality, your closing costs will also vary based on:

Taxes and fees where you live (like transfer taxes and recording fees)

Service costs for things like title and attorney work in your local area

While the home price is obviously going to matter, state laws, tax rates, and even the going costs for title and attorney services can change what you expect to pay. That’s why it's important to talk to the pros ahead of time so you know what to budget for. It can put you in control before you even start shopping.

To give you a rough ballpark, here’s a state-by-state look at typical closing costs right now based on those factors for the median-priced home in each state (see map below):

As the map shows, in some states, typical closing costs are just roughly $1-3K. In a few places, they can be closer to $10-15K. That’s a big swing, especially if you’re buying your first home. And that’s why knowing what to expect matters.

If you want a real number to help with your budget, your best bet is to talk to a local agent and a lender. They can run the math for your price range, loan type, and exact location.

And just in case you’re looking at your state’s number and wondering if there’s any way to trim that bill, NerdWallet shares a few strategies that can help:

Negotiate with the seller. Ask for concessions like a credit toward your closing costs.

Shop around for homeowner’s insurance. Compare coverage and rates before you commit.

Check for assistance programs. Some states, professions, and neighborhoods offer help. Your agent and lender can point you to what’s available locally.

Closing costs are a key part of buying a home, but they can vary more than most people realize. Knowing your numbers (and how to potentially bring them down) can go a long way and help you feel confident about your purchase.

Let’s look at typical closing costs in our area and get you a personalized estimate, so you can craft your ideal budget.

For the past couple of years, it’s been tough for a lot of homebuyers to make the numbers work. Home prices shot up. Mortgage rates too. And a number of people hit pause because it just didn’t feel possible. Maybe you were one of them.

But there’s some encouraging news. If you’ve been waiting for a better time to jump back in, affordability may finally be showing signs of improvement this fall.

The latest data from Redfin shows the typical monthly mortgage payment has been coming down, and is now about $290 lower than it was just a few months ago (see graph below):

And here’s why this is happening. The cost of buying a home really comes down to three things:

Mortgage rates

Home prices

Your wages

Right now, all three are finally moving in a better direction for you. While that doesn’t mean it’s suddenly easy to buy at today’s rates and prices, it does mean it’s not as challenging.

Mortgage rates have come down compared to earlier this year. In May, they were roughly 7%. And now, they’re closer to 6.3% (see graph below):

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

And for some people, that’s been enough to make buying a home possible again. As Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explained on September 10th:

“The downward rate movement spurred the strongest week of borrower demand since 2022 . . . Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year’s pace.”

After several years of prices rising very rapidly, price growth has finally slowed. As Odeta Kushi, Deputy Chief Economist at First American, puts it:

“National home price growth remains positive, but muted — low single digits — and we expect this trend to continue in the second half of the year.”

For buyers, that’s actually a big relief. That moderation makes it easier to plan your budget. And in some markets, prices have even dipped slightly. If you're in one of the markets, you may be able to find something that’s more affordable than you'd expect.

According to the Bureau of Labor Statistics (BLS), wages are up near 4% annually. Lawrence Yun, Chief Economist at NAR, explains why that number is so important right now:

“Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”

In other words, the typical paycheck is rising faster than home prices right now, which helps make buying a little more affordable. Now, it’s not a big difference, but in a market like this, every bit counts.

Lower rates, slower price growth, and stronger wages might be enough to make the numbers finally work for you this fall.

While affordability is still tight, it’s a little easier on your wallet to buy now than it was just few months ago. Remember, data from Redfin shows the typical monthly mortgage payment is already around $290 lower than it was earlier this year.

Have you been wondering if it’s worth taking another look at buying?

Let’s run the numbers together. We can go over your budget, see what’s changed, and figure out if this fall is the time to turn window-shopping into key-turning.

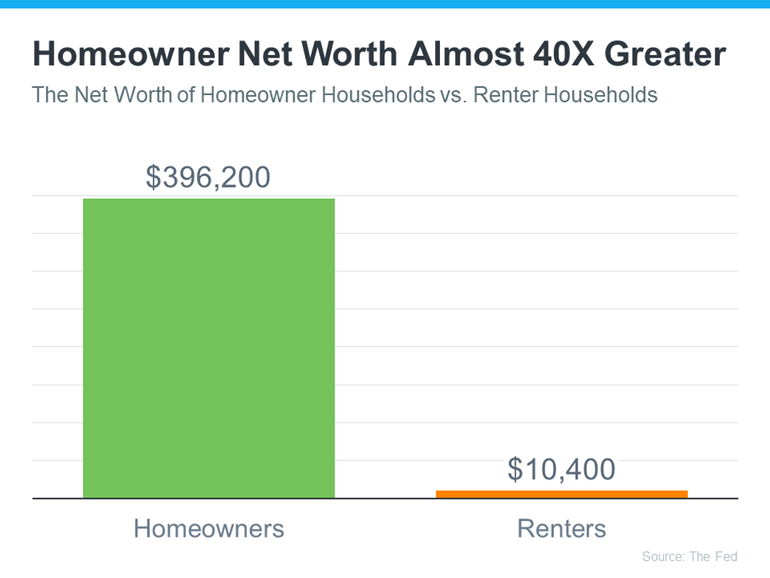

Want to know something important you probably don’t have a professional check for you nearly as often as you should? Spoiler alert: it’s the value of your home.

Because here’s the reality. Your house is likely the biggest financial asset you have. And if you’ve lived in it for a few years or more, chances are it’s been quietly building wealth for you in the background – even if you haven’t been keeping tabs on it.

You might be surprised by just how much it’s grown, even as the market has shifted over the past few months.

That hidden wealth in your home is called equity. It’s the difference between what your house is worth today and what you still owe on your mortgage. Your equity grows over time as home values rise and as you make your monthly payments. Here’s an example to help you really understand how the math works.

Let’s say your house is now worth $500,000, and you have $200,000 left to pay off on your loan. That means you have $300,000 in equity. And that’s right in line with what the typical homeowner has right now.

According to Cotality, the average homeowner with a mortgage has about $302,000 in equity.

Here are the two main reasons homeowners like you have near record amounts of equity right now:

1. Significant Home Price Growth. According to the Federal Housing Finance Agency (FHFA), home prices have jumped by nearly 54% nationwide over the last five years (see map below):

This means your house is likely worth much more now than when you first bought it, thanks to how much prices have climbed over time. And if you’re worried because you’ve heard prices are flattening or even coming down in some markets, just know if you’ve been in your house for a few years (or more) you very likely have enough equity to sell and still come out ahead.

2. People Are Living in Their Homes Longer. Data from the National Association of Realtors (NAR), shows the average homeowner stays in their home for about 10 years now (see graph below):

That’s longer than it used to be. And over that decade? You’ve built equity just by making your mortgage payments and riding the wave of rising home values. Because the financial side of homeownership is about playing the long game, not worrying about little ups and downs in the market here and there. And over time, that means you’re winning.

So, if you’re one of those people who’s been in their home for a bit, here’s how much the behind-the-scenes price growth has helped you out. According to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

Your equity isn’t just a number. It’s a tool you can use to unlock your next big move. Depending on your goals, you could:

Use it to help buy your next home. Your equity could help you cover the down payment on your next home. In some cases, it might even mean you can buy your next house in all cash.

Renovate your current house to better suit your life now. And, if you’re strategic about your projects, they could add even more value to your home if you do sell later on.

Start the business you’ve always dreamed of. Your equity could be exactly what you need for startup costs, equipment, software, or marketing. And that could help increase your earning potential, so you’re getting yet another financial boost.

Chances are, your house is worth quite a bit right now. If you’re curious about the value of your home, let’s connect. We’ll run the numbers and give you a professional equity assessment report, so you know what you’re working with and where you can go from here.

If buying a home is on your radar – even if it’s more of a someday plan than a right now plan – getting pre-approved early is still one of the smartest moves you can make. Why? Because, like anything in life, the right prep work makes things clearer.

The best time to get serious about buying is before you’re ready to buy. Here’s why.

One of the biggest benefits of pre-approval is how it helps you understand your buying power. As part of the pre-approval process, a lender will walk through your finances and tell you what you can borrow based on your income, debts, credit score, and more. That number is power.

Once you have that clarity, you’re no longer guessing. You know what you’re working with. And that gives you the information you need to be able to plan ahead. That way, you’re not falling in love with homes that are outside of your price range – or missing out on ones that aren’t.

You don’t have to be ready to buy to be ready to buy.

It happens all the time – someone scrolls through listings just for fun, and then BAM – they fall in love with something they see online. But by the time they scramble to connect with an agent and then get pre-approved with a lender, someone else beats them to it, and they lose the home. And you don’t want that to happen to you.

While you can’t control when the right home shows up – you can be ready for it.

Pre-approval isn’t about jumping the gun or rushing your timeline. It’s about making sure you’re ready when it’s go-time. As Experian explains:

“…Waiting too long to get a preapproval, however, could leave you at a disadvantage . . . you could find the perfect home, but another buyer could snatch it up while you're waiting for the lender to review your preapproval application. . . getting a preapproval just before you begin actively looking at homes may be your best option.”

Instead of rushing to figure out your numbers, trying to get documentation for your home loan together, and watching the house you love slip away while you wait to hear from your lender, you’re already in the game.

It’s like showing up to the starting line with your shoes tied and your warm-up done – while everyone else is still looking for parking.

But pre-approvals do have an expiration date, so be sure to ask your lender how long it’s good for. Bankrate offers this insight:

“…Many mortgage preapprovals are valid for 90 days, though some lenders will only authorize a 30- or 60-day preapproval. If your preapproval expires, getting it renewed can be as simple as your lender rechecking your credit and finances to ensure there have been no major changes to your situation since the first time ‘round.”

The thing is, if you’ve been pre-approved – even if you’re just thinking about casually looking – you have a much better sense of how to navigate your home search within your budget. Plus, you’ll be ready if the perfect home comes along. So why not make it happen?

Getting pre-approved doesn’t mean you have to buy a house today. But it does mean you’ll know what you’re working with when the right one shows up. If you want to get pre-approved, connect with a lender to get that process started.

In the meantime, let’s have a conversation about what’s on your mind and what you’re looking for.

If the perfect house popped up tomorrow, would you be ready to make a move?

Lately, it feels like a lot of people have been asking the same question: “Is the housing market about to crash?”

If you’ve been scrolling through social media or watching the news, you might have seen some pretty scary headlines yourself. That’s why it’s no surprise that, according to data from Clever Real Estate, 70% of Americans are worried about a housing crash in 2025.

But before you hit pause on your plans to buy or sell a home, take a deep breath. The truth is: the housing market isn’t about to crash – it’s just shifting. And that shift actually works in your favor.

Mark Fleming, Chief Economist at First American, says:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

Think about it. If there’s a shortage of something – like tickets to a popular concert – prices go up. That’s what’s been happening with homes. We still have a shortage of supply. Too many buyers and not enough homes push prices higher.

Check out the white line for 2025 in the graph below. Even though the number of homes for sale is climbing, data from Realtor.com shows we’re still well below normal levels (shown in gray):

That ongoing low supply is what’s stopping home prices from dropping at the national level. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“… if there’s a shortage, prices simply cannot crash.”

And, as more homes become available, that takes some of the intense upward pressure off home price growth – leading to healthier price appreciation.

So, while prices aren’t falling nationally, growing inventory means they also aren’t rising as fast as they were. What we’re seeing is price moderation (see graph below):

And according to Freddie Mac, that moderation should continue through the rest of this year:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

Put simply, that means prices will continue going up in most areas, just not as quickly. That’s good news for anyone who’s been having trouble finding a home and feeling sticker shock from the rapid price appreciation of the past few years.

But of course, what’s happening with prices and inventory is going to vary by local market. So, talk to your agent to find out what’s happening where you live.

Don’t let the talk scare you. Experts agree that a housing market crash is unlikely in 2025. As Business Insider reports:

“. . . economists who study housing market conditions generally do not expect a crash in 2025 or beyond unless the economic outlook changes.”

Instead, we’re heading into a housing market that’s healthier and more balanced, with slower price growth and more opportunity. Let’s chat about what’s happening in our local market and how you can make the most of it.

If buying a home is on your radar – even if it’s more of a someday plan than a right now plan – getting pre-approved early is still one of the smartest moves you can make. Why? Because, like anything in life, the right prep work makes things clearer.

The best time to get serious about buying is before you’re ready to buy. Here’s why.

One of the biggest benefits of pre-approval is how it helps you understand your buying power. As part of the pre-approval process, a lender will walk through your finances and tell you what you can borrow based on your income, debts, credit score, and more. That number is power.

Once you have that clarity, you’re no longer guessing. You know what you’re working with. And that gives you the information you need to be able to plan ahead. That way, you’re not falling in love with homes that are outside of your price range – or missing out on ones that aren’t.

You don’t have to be ready to buy to be ready to buy.

It happens all the time – someone scrolls through listings just for fun, and then BAM – they fall in love with something they see online. But by the time they scramble to connect with an agent and then get pre-approved with a lender, someone else beats them to it, and they lose the home. And you don’t want that to happen to you.

While you can’t control when the right home shows up – you can be ready for it.

Pre-approval isn’t about jumping the gun or rushing your timeline. It’s about making sure you’re ready when it’s go-time. As Experian explains:

“…Waiting too long to get a preapproval, however, could leave you at a disadvantage . . . you could find the perfect home, but another buyer could snatch it up while you're waiting for the lender to review your preapproval application. . . getting a preapproval just before you begin actively looking at homes may be your best option.”

Instead of rushing to figure out your numbers, trying to get documentation for your home loan together, and watching the house you love slip away while you wait to hear from your lender, you’re already in the game.

It’s like showing up to the starting line with your shoes tied and your warm-up done – while everyone else is still looking for parking.

But pre-approvals do have an expiration date, so be sure to ask your lender how long it’s good for. Bankrate offers this insight:

“…Many mortgage preapprovals are valid for 90 days, though some lenders will only authorize a 30- or 60-day preapproval. If your preapproval expires, getting it renewed can be as simple as your lender rechecking your credit and finances to ensure there have been no major changes to your situation since the first time ‘round.”

The thing is, if you’ve been pre-approved – even if you’re just thinking about casually looking – you have a much better sense of how to navigate your home search within your budget. Plus, you’ll be ready if the perfect home comes along. So why not make it happen?

Getting pre-approved doesn’t mean you have to buy a house today. But it does mean you’ll know what you’re working with when the right one shows up. If you want to get pre-approved, connect with a lender to get that process started.

In the meantime, let’s have a conversation about what’s on your mind and what you’re looking for.

If the perfect house popped up tomorrow, would you be ready to make a move?

You may have seen talk online that new home inventory is at its highest level since the crash. And if you lived through the crash back in 2008, seeing new construction is up again may feel a little scary.

But here’s what you need to remember: a lot of what you see online is designed to get clicks. So, you may not be getting the full story. A closer look at the data and a little expert insight can change your perspective completely.

While it’s true the number of new homes on the market hit its highest level since the crash, that’s not a reason to worry. That’s because new builds are just one piece of the puzzle. They don’t tell the full story of what’s happening today.

To get the real picture of how much inventory we have and how it compares to the surplus we saw back then, you’ve got to look at both new homes and existing homes (homes that were lived in by a previous owner).

When you combine those two numbers, it’s clear overall supply looks very different today than it did around the crash (see graph below):

So, saying we’re near 2008 levels for new construction isn't the same as the inventory surplus we did the last time.

And here’s some other important perspective you’re not going to get from those headlines. After the 2008 crash, builders slammed on the brakes. For 15 years, they didn’t build enough homes to keep up with demand. That long stretch of underbuilding created a major housing shortage, which we’re still dealing with today.

The graph below uses Census data to show the overbuilding leading up to the crash (in red), and the period of underbuilding that followed (in orange):

Basically, we had more than 15 straight years of underbuilding – and we’re only recently starting to slowly climb out of that hole. But there’s still a long way to go (even with the growth we’ve seen lately). Experts at Realtor.com say it would roughly 7.5 years to build enough homes to close the gap.

Of course, like anything else in real estate, the level of supply and demand is going to vary by market. Some markets may have more homes for sale, some less. But nationally, this isn’t like the last time.

Just because there are more new homes for sale right now, it doesn’t mean we’re headed for a crash. The data shows today’s overall inventory situation is different.

If you have questions or want to talk about what builders are doing in our area, let’s connect.

Reach out if you want a professional assessment on what your house could sell for today.

If buying a home is on your radar – even if it’s more of a someday plan than a right now plan – getting pre-approved early is still one of the smartest moves you can make. Why? Because, like anything in life, the right prep work makes things clearer.

The best time to get serious about buying is before you’re ready to buy. Here’s why.

One of the biggest benefits of pre-approval is how it helps you understand your buying power. As part of the pre-approval process, a lender will walk through your finances and tell you what you can borrow based on your income, debts, credit score, and more. That number is power.

Once you have that clarity, you’re no longer guessing. You know what you’re working with. And that gives you the information you need to be able to plan ahead. That way, you’re not falling in love with homes that are outside of your price range – or missing out on ones that aren’t.

You don’t have to be ready to buy to be ready to buy.

It happens all the time – someone scrolls through listings just for fun, and then BAM – they fall in love with something they see online. But by the time they scramble to connect with an agent and then get pre-approved with a lender, someone else beats them to it, and they lose the home. And you don’t want that to happen to you.

While you can’t control when the right home shows up – you can be ready for it.

Pre-approval isn’t about jumping the gun or rushing your timeline. It’s about making sure you’re ready when it’s go-time. As Experian explains:

“…Waiting too long to get a preapproval, however, could leave you at a disadvantage . . . you could find the perfect home, but another buyer could snatch it up while you're waiting for the lender to review your preapproval application. . . getting a preapproval just before you begin actively looking at homes may be your best option.”

Instead of rushing to figure out your numbers, trying to get documentation for your home loan together, and watching the house you love slip away while you wait to hear from your lender, you’re already in the game.

It’s like showing up to the starting line with your shoes tied and your warm-up done – while everyone else is still looking for parking.

But pre-approvals do have an expiration date, so be sure to ask your lender how long it’s good for. Bankrate offers this insight:

“…Many mortgage preapprovals are valid for 90 days, though some lenders will only authorize a 30- or 60-day preapproval. If your preapproval expires, getting it renewed can be as simple as your lender rechecking your credit and finances to ensure there have been no major changes to your situation since the first time ‘round.”

The thing is, if you’ve been pre-approved – even if you’re just thinking about casually looking – you have a much better sense of how to navigate your home search within your budget. Plus, you’ll be ready if the perfect home comes along. So why not make it happen?

Getting pre-approved doesn’t mean you have to buy a house today. But it does mean you’ll know what you’re working with when the right one shows up. If you want to get pre-approved, connect with a lender to get that process started.

In the meantime, let’s have a conversation about what’s on your mind and what you’re looking for.

If the perfect house popped up tomorrow, would you be ready to make a move?

Cutting out the agent might seem like a smart way to save when you sell your house. But here’s the hard truth.

Last year, homes that sold with an agent went for almost 15% more than those that sold without one.

That gap is pretty hard to ignore. And with more homes on the market to compete with right now, selling on your own is a mistake that’s going to cost you.

A few years ago, you might’ve gotten away with a “For Sale By Owner” (FSBO) sign in your yard, navigating the process on your own. That’s because homes were flying off the market and buyers were pulling out all the stops. But that’s just not the case anymore. With more inventory than we’ve seen in years, we’re not in a “list it and they will come” market anymore. You need professional expertise.

A yard sign and some photos you take on your own won’t cut it.

Right now, the housing market is getting back to what most would consider a more normal balance of buyers and sellers, and that really changes the game. According to Realtor.com, the latest number of listings for sale was the highest it’s been in any month of July since 2019 (see graph below):

And while inventory growth is going to vary by local market, nationally, this graph shows the number of homes for sale is inching back toward normal.

With more listings available, that means buyers can be more selective. They’ll compare your home to others on price, condition, photos, location, and more. If yours doesn’t stand out, it will get skipped over.

Selling today requires the latest pricing strategy, expert prep work, professional marketing, and strong negotiation skills. And if you’re not bringing all of that to the table, chances are, you’re going to feel it in your bottom line.

That’s why even more home sellers are working with agents today. Data from the National Association of Realtors (NAR) shows a record-low percentage of homeowners sold without an agent last year. And the few sellers who tried to sell on their own realized their mistake pretty quickly.

According to Zillow, 21% of homeowners ended up hiring an agent anyway after struggling to sell on their own.

So, why take the risk? With a local pro, you'll have:

Pricing precision to attract buyers and maximize your return

Expert staging and presentation advice to highlight your home’s best features

Pro-level marketing, including the best exposure and access to buyer networks you can’t reach on your own

Skilled negotiation to evaluate offers and navigate inspections, protecting your bottom line

Local market expertise that helps your listing stand out based on what inventory looks like in your area

An agent's expertise isn’t optional anymore. It’s essential.

In a market with more listings and pickier buyers, many sellers who try to sell on their own end up working with an agent anyway. So why not start there?

Let’s connect so you have a pro who knows exactly what it takes to sell your house in today’s market, for the best possible price, without leaving money on the table.

Reach out if you want a professional assessment on what your house could sell for today.

Lately, it feels like a lot of people have been asking the same question: “Is the housing market about to crash?”

If you’ve been scrolling through social media or watching the news, you might have seen some pretty scary headlines yourself. That’s why it’s no surprise that, according to data from Clever Real Estate, 70% of Americans are worried about a housing crash in 2025.

But before you hit pause on your plans to buy or sell a home, take a deep breath. The truth is: the housing market isn’t about to crash – it’s just shifting. And that shift actually works in your favor.

Mark Fleming, Chief Economist at First American, says:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

Think about it. If there’s a shortage of something – like tickets to a popular concert – prices go up. That’s what’s been happening with homes. We still have a shortage of supply. Too many buyers and not enough homes push prices higher.

Check out the white line for 2025 in the graph below. Even though the number of homes for sale is climbing, data from Realtor.com shows we’re still well below normal levels (shown in gray):

That ongoing low supply is what’s stopping home prices from dropping at the national level. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“… if there’s a shortage, prices simply cannot crash.”

And, as more homes become available, that takes some of the intense upward pressure off home price growth – leading to healthier price appreciation.

So, while prices aren’t falling nationally, growing inventory means they also aren’t rising as fast as they were. What we’re seeing is price moderation (see graph below):

And according to Freddie Mac, that moderation should continue through the rest of this year:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

Put simply, that means prices will continue going up in most areas, just not as quickly. That’s good news for anyone who’s been having trouble finding a home and feeling sticker shock from the rapid price appreciation of the past few years.

But of course, what’s happening with prices and inventory is going to vary by local market. So, talk to your agent to find out what’s happening where you live.

Don’t let the talk scare you. Experts agree that a housing market crash is unlikely in 2025. As Business Insider reports:

“. . . economists who study housing market conditions generally do not expect a crash in 2025 or beyond unless the economic outlook changes.”

Instead, we’re heading into a housing market that’s healthier and more balanced, with slower price growth and more opportunity. Let’s chat about what’s happening in our local market and how you can make the most of it.

When selling your house, the price you choose isn’t just a number, it's a strategy. And in today’s market, that strategy needs to be sharp.

The number of homes for sale is climbing. And that means buyers have more choices and can be more selective. If your price doesn’t line up with what else is out there, they’ll scroll right past it and go on to the next one.

Pricing right from the start is your best move – and a great agent can help make sure you do.

And more sellers are finding that out the hard way. They list their house based on how things were a year ago – or based on a neighbor’s sale that happened under completely different circumstances. Then, when their house doesn’t sell, they’re left with three tough choices:

Drop the price: Cutting the price might help get more eyes on the house again, but it can also trigger red flags. Buyers may wonder what’s wrong with it. And that’s going to impact any offers you get after the price cut.

Take it off the market: Some sellers give up on the idea of selling right now. The worst part about this is it means putting their future plans on the back burner. That dream of more space, downsizing, or relocating? On pause.

Rent it out: Others go the landlord route, but managing tenants and navigating leases isn’t always the simple fallback it seems. Renting can work, but it’s often a lot more hassle than people expect.

None of those options were part of the original plan. And honestly, none of them are where you should end up if you wanted to sell. Here’s a look at how a local agent’s expertise can help you avoid these headaches. Let's use price cuts as an example.

While the number of price cuts is up nationally, data shows some parts of the country are seeing far more of them than others. It all comes down to how much inventory has grown in that area (see map below):

As Realtor.com explains:

“Regionally, price reductions in June were significantly more common in the South and West (23% of listings) than they were in the Northeast (13% of listings), reflecting the inventory divergence across these regions.”

That means pricing isn’t one-size-fits-all. What’s happening nationally might not reflect what’s happening in your zip code, and that’s why you shouldn’t try to determine your list price on your own.

A skilled agent doesn’t just toss out a number. As Zillow says:

“Well-priced homes are more likely to sell quickly, but pricing your home to sell quickly and for maximum dollar requires strategy and knowledge of your local market. You need to have a clear-eyed view of your home in relation to the competition, and knowledge about whether you’re in a buyers or sellers market. It also helps to know what buyers in your area can afford.”

And that’s all knowledge your agent will have. They study your local market, compare recent sales, and factor in your goals and buyer behavior. Based on what’s happening where you live, sometimes the best play will be pricing right at current market value. Other times pricing a little lower actually will spark more offers and ultimately get you a better final sale price.

So don’t skimp on the strategy or on your agent. With their local market know-how, you’ll be able to sell quickly, even in a shifting market.

Overpricing can lead to tough choices you never want to face. But with the right price, and the right guidance, you can skip the stress and sell with confidence. Let’s connect so you have a pricing strategy that works for today’s market and gets you where you want to go.

There are plenty of headlines these days calling for a housing market crash. But the truth is, they’re not telling the full story. Here’s what’s actually happening, and what the experts project for home prices over the next 5 years. And spoiler alert – it’s not a crash.

Yes, in some local markets, prices are flattening or even dipping slightly this year as more homes hit the market. That’s normal with rising inventory. But the bigger picture is what really matters, and it’s far less dramatic than what the doom-and-gloom headlines suggest. Here’s why.

Over 100 leading housing market experts were surveyed in the latest Home Price Expectations Survey (HPES) from Fannie Mae. Their collective forecast shows prices are projected to keep rising over the next 5 years, just at a slower, healthier pace than what we’ve seen more recently. And that kind of steady, sustainable growth should be one factor to help ease your fears about the years ahead (see graph below):

And if you take a look at how the various experts responded within the survey, they fall into three main categories: those that were most optimistic about the forecast, most pessimistic, and the overall average outlook.

Here’s what the breakdown shows:

The average projection is about 3.3% price growth per year, through 2029.

The optimists see growth closer to 5.0% per year.

The pessimists still forecast about 1.3% growth per year.

Do they all agree on the same number? Of course not. But here’s the key takeaway: not one expert group is calling for a major national decline or a crash. Instead, they expect home prices to rise at a steady, more sustainable pace.

That’s much healthier for the market – and for you. Yes, some areas may see prices hold relatively flat or dip a bit in the short term, especially where inventory is on the rise. Others may appreciate faster than the national average because there are still fewer homes for sale than there are buyers trying to purchase them. But overall, more moderate price growth is cooling the rapid spikes we saw during the frenzy of the past few years.

And remember, even the most conservative experts still project prices will rise over the course of the next 5 years. That’s also because foreclosures are low, lending standards are in check, and homeowners have near record equity to boost the stability of the market. Together, those factors help prevent a wave of forced sales, like the kind that could drag prices down. So, if you’re waiting for a significant crash before you buy, you might be waiting quite a long time.

If you’ve been on the fence about your plans, now’s the time to get clarity. The market isn’t heading for a crash. It’s on track for steady, slow, long-term growth overall, with some regional ups and downs along the way.

Want to know what that means for our neighborhood? Because national trends set the tone, but what really matters is what’s happening in your zip code. Let’s have a quick conversation so you can see exactly what our local data means for you.

If you’ve seen headlines saying home sales are down compared to last year, you might be thinking – is it even a good time to sell?

Here’s the thing. Sure, the pace of the market has cooled compared to the frenzy we saw just a few years ago, but that’s not a red flag. It’s a return to normal. And normal doesn’t mean nothing’s happening. Buyers are still out there – and homes are still selling.

Why? Because real life doesn’t pause for perfect conditions. There are always people who need to buy – and this year is no exception. Buyers who are in the middle of a big change in their lives, a new marriage, a growing family, or a new job still need to move, no matter where mortgage rates are. And they may be looking for a home just like yours.

Let’s break it down using the latest sales data from the National Association of Realtors (NAR). Based on the current pace, we’re on track to sell 4.03 million homes this year (not including new construction).

That means in the time it takes to read this, another 8 homes will sell. Let that sink in. Every minute, buyers are making moves – and sellers are closing deals.

If you’ve been holding off on selling your house because you think buyers aren’t out there, let this reassure you – there are still buyers looking to buy.

But since the market is balancing out, selling today takes more than just putting up a sign in the yard. You’ve got to price your house right, market it well, and know how to reach the buyers who are ready to act. That’s where a trusted local agent comes in.

They’ll help you navigate this market, position your home to stand out, and guide you through every step.

The market hasn’t stopped. Buyers are still buying. Life is still happening. And if selling your home is part of your next chapter, let’s make it happen.

Roughly 11,000 homes are selling every day – and yours could be next. When you’re ready to take the next step, let’s connect.

Let’s connect to get you there.

Headlines are saying home prices are starting to dip in some markets. And if you’re beginning to second guess your plans based on what you’re hearing in the media, here’s what you need to know.

It's true that a few metros are seeing slight price drops. But don't let that overshadow this simple truth. Home values almost always go up over time (see graph below):

While everyone remembers what happened around the housing crash of 2008, that was the exception – not the rule. It hadn’t happened before, and hasn’t since. There were many market dynamics that were drastically different back then, too. From relaxed lending standards to a lack of homeowner equity, and even a large oversupply of homes, it was very different from where the national housing market is today. So, every headline about prices slowing down, normalizing, or even dipping doesn’t need to trigger fear that another big crash is coming.

Here’s something that explains why short-term dips usually aren’t a long-term deal-breaker.

In real estate, you might hear talk about the five-year rule. The idea is that if you plan to own your home for at least five years, short-term dips in prices usually don’t hurt you much. That’s because home values almost always go up in the long run. Even if prices drop a bit for a year or two, they tend to bounce back (and then some) over time.

Take it from Lance Lambert, Co-Founder of ResiClub:

“. . . there’s the ‘five-year rule of thumb’ in real estate—which suggests that most buyers can buffer themselves from mild short-term declines if they plan to own a property for at least that amount of time.”

Here’s something else to put your mind at ease. Right now, most housing markets are still seeing home prices rise – just not as fast as they were a few years ago.

But in the major metros where prices are starting to cool off a little (the red bars in the graph below), the average drop is only about -2.9% since April 2024. That’s not a major decline like we saw back in 2008.

And when you look at the graph below, it’s clear that prices in most of those markets are up significantly compared to where they were five years ago (the blue bars). So, those homeowners are still ahead if they’ve been in their house for a few years or more (see graph below):

Over the past 5 years, home prices have risen a staggering 55%, according to the Federal Housing Finance Agency (FHFA). So, a small short-term dip isn’t a significant loss. Even if your city is one where they’re down 2% or so, you’re still up far more than that.

And if you break those 5-year gains down even further, using data from the FHFA, you’ll see home values are up in every single state over the last five years (see map below):

That’s why it’s important not to stress too much about what’s happening this month, or even this year. If you’re in it for the long haul (and most homeowners are) your home is likely to grow in value over time.

Yes, prices can shift in the short term. But history shows that home values almost always go up – especially if you live there for at least five years. So, whether you’re thinking of buying or selling, remember the five-year rule, and take comfort in the long view.

When you think about where you want to be in five years, how does owning a home fit into that picture?

Let’s connect to get you there.

Do you think a brand-new home means a bigger price tag? Think again.

Right now, something unique is happening in the housing market. According to the Census and the National Association of Realtors (NAR), the median price of newly built homes is actually lower than the median price for existing homes (ones that have already been lived in):

You read that right. That brand new, never-been-lived-in house may cost less than the one built 20 years ago in a neighborhood just down the street. So, if you wrote off a new build because you assumed they’d be financially out of reach, here’s what you should know. You could be missing out on some of the best options in today’s housing market.

1. Builders Are Building Smaller Homes

Builders know that buyers are struggling with affordability today. So, instead of building big houses that may not sell, they’re building smaller ones that will. According to the Census, the average size of a newly built single-family home has dropped considerably over the past few years (see graph below):

And as size goes down, the price often does too. Smaller homes use fewer materials, which makes them less expensive to build. That helps builders keep prices lower so more people can afford them.

2. Builders Are Offering Price Cuts and Incentives

In May, according to the National Association of Home Builders (NAHB), 34% of builders lowered their prices, with an average price drop of 5%. That’s because they want to be sure they’re selling the inventory they have before they build more.

On top of that, 61% of builders also offered sales incentives – like helping with closing costs or buying down your mortgage rate. These are all ways builders are making their homes more affordable, so these homes sell in today’s market.

If you're trying to buy a home right now, be sure to talk to your agent to find out what builders are doing in and around your area. They can find new home communities, as well as builders who are offering incentives or discounts, and hidden gems you might not uncover on your own.

Plus, buying a newly built home often means there are different steps in the process than if you purchase a home that’s been lived in before. That’s why it’s so important to have your own agent who can explain the fine print. You want a pro in your corner to advocate for you, negotiate on your behalf, and make sure your best interests come first.

You could get a home that’s brand new, with modern features, at a price that’s even lower than some older homes. Let’s talk about what you’re looking for and see if a newly built home is the right fit for you.

If buying a home is on your to-do list, what would stop you from exploring newly built options?

Whether you’re planning to move soon or not, it’s smart to be strategic about which home projects you take on. Your time, energy, and money matter – and not all upgrades offer the payoff you might expect. As U.S. News Real Estate explains:

". . . not every home renovation project will increase the resale value of a home. Before you invest in a swimming pool or new addition, you should consider whether the project will pay itself off by getting prospective buyers in the door when it’s time to sell."

That’s why, before you pick up a power tool or call a contractor, your first step should be talking to a local agent.

If you plan to move relatively soon, you’ll want to get a jump start on your to-do list. And even if moving isn’t on your radar yet, life can change quickly – and a new job, a growing family, or shifting priorities can fast-track your plans. You don’t want to be scrambling to fix up your home if your timeline changes.

Smart updates now = fewer headaches later.

By planning ahead, you can spread out the work over time, which is easier on your wallet and your stress levels. Plus, you’ll get to enjoy the upgrades while you’re still living there and have the peace of mind your house is ready to impress when it's time to list.

If you’re not sure which projects are worth your time and money – here's some information that can help. A study from the National Association of Realtors (NAR) shows which upgrades typically offer the best return on your investment (ROI) (see graph below):

If an update you're already thinking about overlaps with those high-ROI upgrades, great. Odds are it'll improve your quality of life now and your home’s value later.

But don’t take this list as law. This is based on national data and is the sort of thing that's going to vary based on what’s most sought-after where you live. That’s where your agent comes in. As an article from Ramsey Solutions says:

“The best way to gauge what you can expect in terms of resale value on home improvements—especially if you’re planning to sell soon—is to talk to a real estate agent who is an expert in your market. They’re sure to know the local trends, and they can show you how other homes with the features you want to add are selling. That way, you can make an educated decision before you start ordering lumber and knocking down walls.”

You'll just want to make sure you don't overdo it. Too many high-end updates can make your home the priciest in the neighborhood. That might sound great, but it can actually turn buyers away if it's outside their expected price range for the area. The right agent will help you make smart updates that buyers will love, without going overboard.

Whether the project is big or small, it pays to be strategic. And an agent is a key piece of that strategy.

It doesn’t matter whether you plan to move soon or not, it can still pay off to make strategic updates that’ll help you love your home now and stand out later.

What’s one upgrade you’ve been thinking about – and wondering if it’s worth it? Let’s make sure it’ll pay off when the time comes.

If you're a first-time homebuyer, chances are you'll come across some terms you’re not familiar with. And that can be overwhelming, especially while going through one of the biggest purchases of your life.

The good news is you don’t need to be an expert on real estate jargon. That’s your agent’s job. But getting to know these basic terms will help you feel a lot more confident throughout the process.

Once you’re familiar with this terminology, you’ll have a better understanding of important details – from contracts to negotiations. So, when those big conversations happen, you’ll feel informed, in control, and able to make the best decision for your unique situation. As Redfin puts it:

“Having a basic understanding of important real estate concepts before you start the homebuying process will give you peace of mind now and could save you a fortune in the future.”

Here’s a breakdown of a few key real estate terms and definitions you should know, according to the Federal Trade Commission (FTC) and First American.

Appraisal: A report providing the estimated value of the home. Lenders rely on appraisals to determine a home’s value, so they’re not lending more than it’s worth.

Contingencies: Contract conditions that must be met, typically within a certain timeframe or by a specified date. For example, a home inspection is a common contingency. While you can waive these to try and make your offer more competitive, it’s generally not recommended.

Closing Costs: A collection of fees and payments made to the various parties involved in your home purchase. Ask your lender for a list of closing cost items, including attorney’s fees, taxes, title insurance, and more.

Down Payment: This varies by buyer, but is typically 3.5-20% of the purchase price of the home. There are even some 0% down programs available. Ask your lender for more information. Chances are, unless specified by your loan type of lender, you don’t need to put 20% down.

Escalation Clause: This is typically used in highly competitive markets. It’s an optional add on in a real estate contract that says a potential buyer is willing to raise their offer on a home if the seller receives a higher competing offer. The clause also includes how much a buyer is willing to pay over the highest offer.

Mortgage Rate: The interest rate you pay when you borrow money to buy a home. Consult a lender so you know how it can impact your monthly mortgage payment.

Pre-Approval Letter: A letter from a lender that shows what they’re willing to lend you for your home loan. This, plus an understanding of your savings, can help you decide on your target price range. Getting this from a lender should be one of your first steps in the homebuying process, before you even start browsing homes online.

You don't need to have all these terms memorized, but a little knowledge goes a long way. Brushing up on the basics now means fewer surprises later – and more clarity when you buy a home.

What unfamiliar real estate term or phrase have you come across that wasn’t on this list?

Let’s connect and talk through it so you have a solid understanding of what it means and where it may show up in the homebuying process.

Whether you’re planning to move soon or not, it’s smart to be strategic about which home projects you take on. Your time, energy, and money matter – and not all upgrades offer the payoff you might expect. As U.S. News Real Estate explains:

". . . not every home renovation project will increase the resale value of a home. Before you invest in a swimming pool or new addition, you should consider whether the project will pay itself off by getting prospective buyers in the door when it’s time to sell."

That’s why, before you pick up a power tool or call a contractor, your first step should be talking to a local agent.

If you plan to move relatively soon, you’ll want to get a jump start on your to-do list. And even if moving isn’t on your radar yet, life can change quickly – and a new job, a growing family, or shifting priorities can fast-track your plans. You don’t want to be scrambling to fix up your home if your timeline changes.

Smart updates now = fewer headaches later.

By planning ahead, you can spread out the work over time, which is easier on your wallet and your stress levels. Plus, you’ll get to enjoy the upgrades while you’re still living there and have the peace of mind your house is ready to impress when it's time to list.

If you’re not sure which projects are worth your time and money – here's some information that can help. A study from the National Association of Realtors (NAR) shows which upgrades typically offer the best return on your investment (ROI) (see graph below):

If an update you're already thinking about overlaps with those high-ROI upgrades, great. Odds are it'll improve your quality of life now and your home’s value later.

But don’t take this list as law. This is based on national data and is the sort of thing that's going to vary based on what’s most sought-after where you live. That’s where your agent comes in. As an article from Ramsey Solutions says:

“The best way to gauge what you can expect in terms of resale value on home improvements—especially if you’re planning to sell soon—is to talk to a real estate agent who is an expert in your market. They’re sure to know the local trends, and they can show you how other homes with the features you want to add are selling. That way, you can make an educated decision before you start ordering lumber and knocking down walls.”

You'll just want to make sure you don't overdo it. Too many high-end updates can make your home the priciest in the neighborhood. That might sound great, but it can actually turn buyers away if it's outside their expected price range for the area. The right agent will help you make smart updates that buyers will love, without going overboard.

Whether the project is big or small, it pays to be strategic. And an agent is a key piece of that strategy.

It doesn’t matter whether you plan to move soon or not, it can still pay off to make strategic updates that’ll help you love your home now and stand out later.

What’s one upgrade you’ve been thinking about – and wondering if it’s worth it? Let’s make sure it’ll pay off when the time comes.

With all the uncertainty in the economy, the stock market has been bouncing around more than usual. And if you’ve been watching your 401(k) or investments lately, chances are you’ve felt that pit in your stomach. One day it’s up. The next day, it’s not. And that may make you feel a little worried about your finances.

But here’s the thing you need to remember if you’re a homeowner. According to Investopedia:

“Traditionally, stocks have been far more volatile than real estate. That's not to say that real estate prices aren't ever volatile—the years around the 2007 to 2008 financial crisis are just one memorable example—but stocks are more prone to large value swings.”

While your stocks or 401(k) might see a lot of highs and lows, home values are much less volatile.

Take a look at the graph below. It shows what happened to home prices (the blue bars) during past stock market swings (the orange bars):

Even when the stock market falls more substantially, home prices don’t always come down with it.

Big home price drops like 2008 are the exception, not the rule. But everyone remembers that one. That stock market crash was caused by loose lending practices, subprime mortgages, and an oversupply of homes – a scenario that doesn’t exist today. That’s what made it so different.

In many cases before and after that time, home values actually went up while the stock market went down, showing that real estate is generally much more stable.

This graph shows how stock prices go up and down (the orange line), sometimes by more than 30% in a year. In contrast, home prices (the blue line) change more slowly (see graph below):

Basically, stock values jump around a lot more than home prices do. You can be way up one day and way down the next. Real estate, on the other hand, isn’t usually something that experiences such dramatic swings.

That’s why real estate can feel more stable and less risky than the stock market.

So, if you’re worried after the recent ups and downs in your stock portfolio, rest assured, your home isn’t likely to experience the same volatility.

And that’s why homeownership is generally viewed as a preferred long-term investment. Even if things feel uncertain right now, homeowners win in the long run.

A lot of people are feeling nervous about their finances right now. But there’s one reason for you to feel more secure – your investment in something that’s stood the test of time: real estate.

Last year, 70% of buyers abandoned their home search – and maybe you were one of them. It makes sense. Inventory was low, prices were high, and mortgage rates were up and down like a rollercoaster. All of that made it really hard to find a home you loved – and could afford.

But guess what? The market is shifting.

So, if you paused your moving plans in 2024, it might be time to hit play again. Here’s why.

Even if you could make the numbers work, the lack of available homes in recent years probably made it hard to come by something that fit your needs. But inventory is rising, which means you have more options now.

According to Realtor.com, inventory has jumped 27.5% since this time last year (see graph below):

So, if you were reluctant to list your house because you weren’t sure where you’d go if it sold, you have more choices than you did a year ago. That’s a big win.

When the supply of homes for sale is low, they’re snatched up quickly because there just aren't enough of them to go around. And a few years ago, that meant your house could sell overnight. While that’s not always a bad thing, if you’re planning a move and also need to find your next home, a slower pace isn’t the end of the world. In fact, it’s welcome relief.

Now that inventory has grown, homes are staying on the market longer, meaning you don’t have to feel as rushed in the process (see graph below):

The latest data shows the typical time homes spent on the market went up by about 8% this year – that’s higher than we’ve seen since 2020, but still a faster pace than before the market ramped up. And it’s about a week longer than last year. Talk about a sweet spot for movers. It may seem like just a few days, but it gives you more flexibility and time to be thoughtful about your decisions. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, notes:

And if you’re thinking – but wait – doesn’t that mean it will be harder to sell my house? Don’t worry. With inventory still almost 23% below the pre-pandemic norm, well-priced homes are selling, especially as more buyers step back into the game this season.

With growing inventory, sellers who want to upgrade, downsize, or relocate have more choices. Plus, with less pressure to rush into an offer, it could be a great time to revisit your home search if you’ve put it on hold.

“There are more homes for sale than in the last few years, which means the market pace is a bit more manageable–with longer days on market–and many sellers are more flexible . . . Though buyers face still-high housing costs, they may find a bit more give in the market, which could give them more time to make a decision, even in the busy spring and summer months.”

With more homes on the market and more time to make decisions, what else do you need to see in order to kickstart your home search again? Let’s talk about what’s happening in our local market right now.

Spring is in full swing, and the housing market is picking up along with it. And if you’ve been wondering whether now is the right time to buy or sell, here’s the inside scoop on why this spring may be a great time to make your move.

After a long stretch of tight inventory, the number of homes for sale is finally improving. According to recent national data from Realtor.com, active listings are up 27.5% compared to this time last year.

Look at the graph below and follow the green line for 2025. You can see, even though inventory levels still haven’t returned to pre-pandemic norms (shown in gray), that number is higher than it has been going into the spring market over the past few years (see graph below):

Buyers: This means you have more choices, and you can be more selective.

Sellers: With more homes available than in recent years, you’re more likely to find what you’re looking for when you move. And knowing that inventory is still below more normal levels means there will be demand for your home when you sell it, too.